USDA raises Malaysia’s palm oil production forecast for MY 2025/26

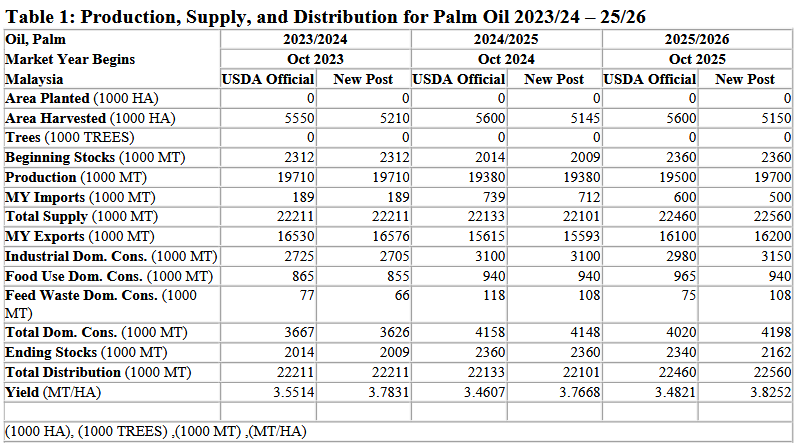

Malaysia’s palm oil sector is set to strengthen in MY 2025/26, with production estimated at 19.7 million tons due to improved weather, higher early-season yields, and expanded effective harvesting areas. Domestic industrial and food-use demand remains steady, while exports to Asia and the Middle East are expected to stay strong, keeping ending stocks at 2.16 million tons.

Malaysia’s palm oil sector is expected to strengthen in marketing year MY 2025/26, supported by improved weather conditions, a larger effective harvested area, and higher early-season fresh fruit bunch (FFB) yields. The USDA has revised its production outlook upward, with output in the opening months of the season ranking among the highest seen over the past four years, boosting overall supply availability.

Palm oil production in MY 2025/26 is now estimated at 19.7 million metric tons, above previous projections. The increase is driven by expanded effective harvesting areas and the normalization of plantation operations following weather-related disruptions in the prior season. In late 2025, key oil palm-growing regions largely avoided widespread flooding, helping to limit losses and support steady harvesting activity.

An additional growth factor is the transition of part of the planted area into full maturity. Estates established in earlier years are moving beyond the immature phase, improving yields without a significant expansion in total planted area. At the same time, replanting rates remain below national targets, which could constrain longer-term productivity gains.

Domestic industrial consumption of palm oil in MY 2025/26 is projected at 3.15 million metric tons. Demand is underpinned by steady activity in the oleochemical, food manufacturing, and biodiesel sectors. Further support comes from continued investment in downstream processing, including renewable fuels and sustainable aviation fuel (SAF) projects.

Food-use consumption of palm oil is also expected to increase, reaching an estimated 940,000 metric tons. Stable demand from food service and food processing industries, along with ongoing use in frying and used cooking oil (UCO) applications, continues to support this segment. Feed and waste use remains relatively small but is gradually rising.

Positive trends are also evident in the palm kernel and palm kernel oil (PKO) segment. Higher kernel recovery rates and increased crushing volumes are driving growth in domestic consumption of palm kernel meal, particularly from the feed sector and expanding livestock, dairy, and cattle projects.

In external trade, Malaysia is expected to maintain its competitive position. Palm oil exports in MY 2025/26 are forecast to remain stable, supported by higher production and firm demand from Asia and the Middle East. Meanwhile, ending stocks are projected to decline to 2.16 million metric tons, indicating that increased domestic use and exports will partially offset gains from higher production and imports.

To Read more about Edible Oil News continue reading Agriinsite.com

Source : Ukr Agro Consult