Less wheat milled to start the new season: Grain market daily

In July 2024, the UK flour milling industry, including starch and bioethanol production, used 9% less wheat than in July 2023, totaling 482.1 Kt, according to AHDB. Usage of home-grown wheat dropped 12%, while imported wheat usage rose by 9% year-on-year, comprising 20% of total wheat usage. The decrease in ‘other flour’ production, a proxy for starch and bioethanol demand, contributed to this drop

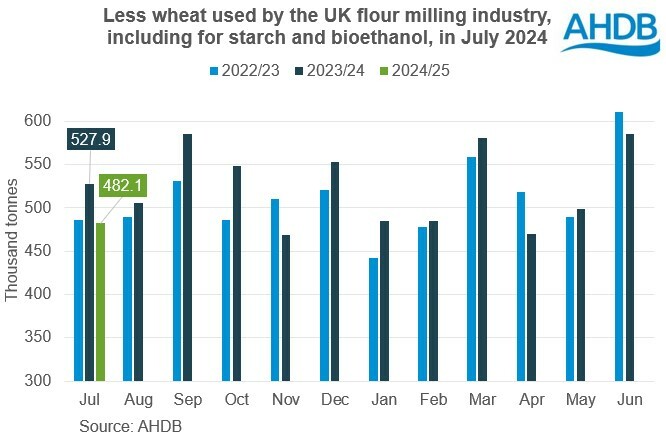

The UK flour milling industry, including for starch and bioethanol production, used 9% less wheat in July 2024 than in July 2023 shows data from AHDB. In July 2024, the first month of the 2024/25 season, the industry used a total of 482.1 Kt of wheat.

Usage of home-grown wheat fell 12% compared with July 2023, while there was a 9% rise in the amount of imported wheat used year-on-year. However, when compared to June 2024, as a proportion of the total wheat used, imported wheat lost a little ground. In July, imported wheat accounted for 20% of all wheat used by, down from 24% in June, though still ahead of July 2023 (17%). The proportion of imported wheat used increased through last season, reflecting both the quality of the 2023 crop and expectations for tight wheat supplies this season.

Last season’s strong wheat import pace is expected to continue this season; HMRC releases data for July next week. The EU Commission reports that the UK is the fifth largest export destination for EU common wheat so far this season. From 1 July – 2 September, the EU shipped 277.7 Kt of common wheat to the UK, up from just 93.2 Kt in the same period last season.

Starch and bioethanol usage drives the drop

The pull back in wheat usage was led by lower ‘other flour’ production, which declined 22% year-on-year in July to 88.5 Kt. ‘Other flour’ production can be used as a rough proxy for demand for wheat from the starch and bioethanol industries. This fall suggests that less wheat was used to produce starch and bioethanol in July, continuing the trend from the end of last season. Towards the end of 2023/24, maize was expected to feature more heavily in usage by the sector due to its price competitiveness against wheat.

Though it has softened a little of late, wheat continues to hold a larger premium over maize than throughout last season. If this price relationship persists, this could dent demand for wheat from the sector. There’s also a risk to demand for home-grown wheat from this sector from the uncertainty over the UK’s future recognition under the EU’s Renewable Energy Directive (RED II).

The UK is expecting a much smaller wheat crop this season following the reduced area, with an increased reliance on imports. However, the level of imports needed will depend on domestic demand and the final crop size so it will be important to monitor the data and policy developments. Defra is scheduled to release the final English crop areas on 26 September and provisional English production estimates on 10 October. The Scottish government usually releases production information in mid-October.

To read more about the news about the Wheat News continue reading Agriinsite.com

Source Link : https://ahdb.org.uk/news/less-wheat-milled-to-start-the-new-season-grain-market-daily